The economic impact of COVID-19 is being felt on a global level, and with specific sectors more severely affected, some may see a quicker bounce back than others once the crisis is over.

Not All Industries Equally Affected

With travel restrictions and social distancing measures in place, mobile communication platforms, e-commerce sites and “home comfort” services have seen a significant increase in demand. Zoom, Netflix, Domino’s and Blue Apron all saw a notable uplift in their stock price index during the month of March.

The crisis is pushing many industries to adapt and adjust rapidly. For example:

- Most schools and universities have closed down but continued operations online, meaning the education sector has experienced a relatively low impact. Analysts predict that online learning will become the “new normal” as education institutions expand their online offerings. Student numbers at online schools have already soared, which is also leading to job creation.

- On the other hand, the property and commercial real estate industry has been significantly impacted by the lockdown. Operators are quickly reacting to offset this by offering virtual tours to help companies gather information and plan the next steps for when restrictions loosen.

When Is The UK Predicted To Recover?

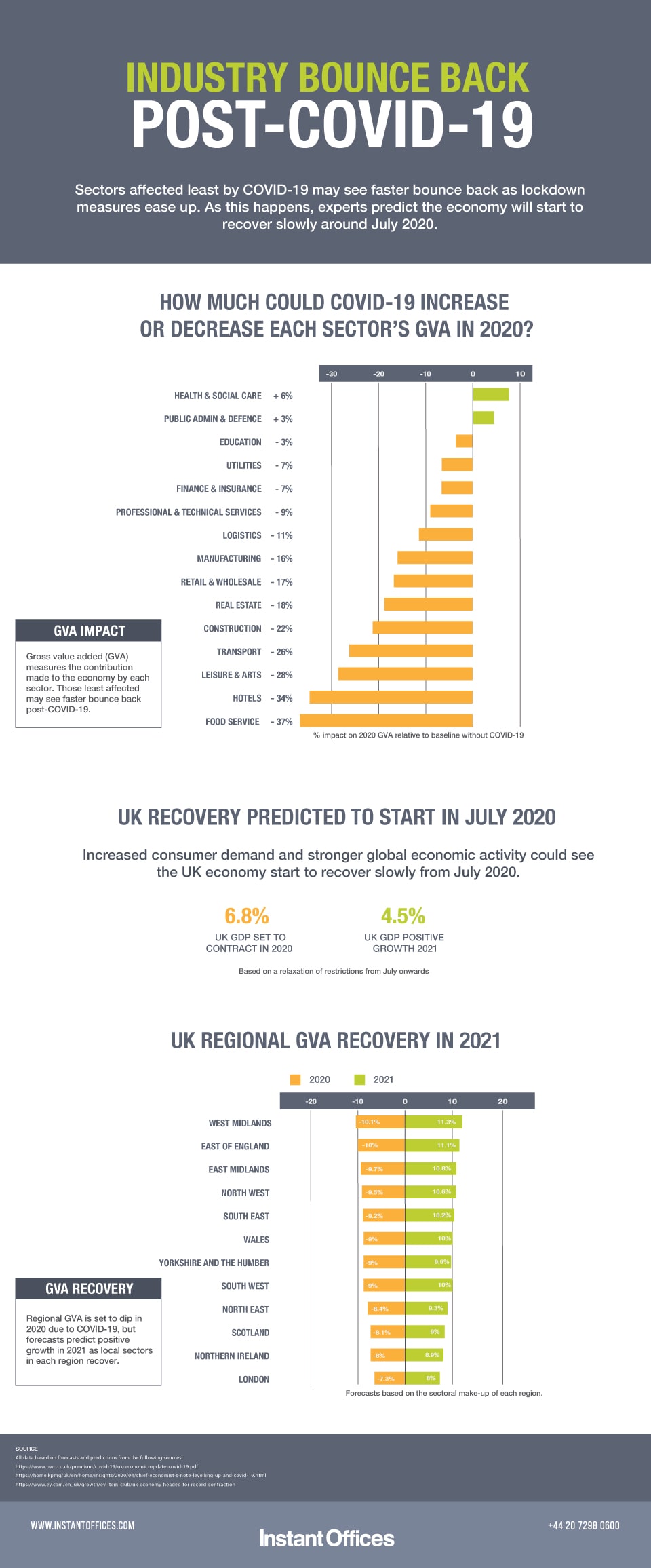

COVID-19 has had a significant impact on all areas of the UK Economy, but the sectors least affected are likely to see faster bounce back as the lockdown measures ease up, and the economy starts to recover.

A report by Ernst & Young originally predicted UK GDP to grow by 1.2% in 2020. Instead, due to COVID-19, it is set to contract by 6.8%. Although this paints a bleak picture right now, there is hope for the latter part of 2020, with forecasts suggesting the economy will slowly start to recover in July (Q3) as restrictions relax.

Some Sectors to Recover Faster than Others

With the country self-isolating and demand dipping to an all-time low, food services, like restaurants and pubs, as well as the hotel and transport sectors, are likely to see the most significant impact to overall productivity and output, resulting in lower economic productivity, or GVA.

On the other hand, education and utilities sectors are less affected, as operations have still largely been able to continue remotely. Due to the high demand for services, health & social care, and public admin sectors are both likely to see increased GVA.

PricewaterhouseCoopers has based estimated GVA impact on two scenarios based on a ‘smooth exit’ or a ‘bumpy exit’ from COVID-19: “In our ‘Smooth exit’ scenario, we estimate reductions of around 14% to 20% in annual 2020 GVA in these sectors relative to a baseline without COVID-19. In our ‘Bumpy exit’ scenario, these sectors could suffer a negative impact on GVA of around 26% to 37% in 2020.”

Regions to See Growth in 2021 as Local Sectors Recover

The recovery rate of various sectors will have a massive impact regionally over the next two years, according to a report by KPMG. Based on the sectoral make-up of each region, London’s GVA is set to be the least affected due to its extensive service-based economy and remote workforce, with a reduction of 7.3% in 2020.

In contrast, the West Midlands is forecast to see GVA reduce by 10.1% due to its sizeable automotive sector. Similarly, in the East of England, slow recovery in its large construction sector will see GVA reduce by 10% this year.

The good news is that the scale of recovery across most regions in 2021 will be similar to contractions in 2020, indicating that as most sectors start to recover, local economies could make up for lost ground.

Recovery Set to Begin in July 2020

The economy is not set to return to its 2019 size until 2023, however slow bounce back is expected across the board as consumer demand increases post-COVID-19, and global economic activity starts to ramp up.

Confidence High Among Professionals in Construction and Healthcare

Based on the LinkedIn Workforce Confidence Index, which asks professionals to rate how confident they feel about their industry two years from now, shows those in construction and healthcare are more confident than the UK average. Scored out of 100, the UK average currently sits at 13, with those in construction at 24, and those in healthcare at 21. The least certain industries right now are media and communications, at 12, and recreation and travel, at -1.

Click to enlarge

Lessons From Post-COVID China

Trends in China are helping to shape our predictions for future bounce-back closer to home. A recent survey on the impact of COVID-19 on Chinese society asked 5,859 respondents aged between 18 and 60 years which industries are likely to recover the fastest after the crisis is over.

The most promising industries for economic recovery are:

| Industry | Vote |

|---|---|

| Medical Education | 38% |

| AI | 36% |

| Internet | 32% |

| e-Commerce | 31% |

| Delivery & Logistics | 25% |

| Health Care | 23% |

| Live Streaming | 22% |

| Scientific Research | 20% |

| Data Services | 19% |

| Software Technology | 19% |

Some Sectors Will Benefit from “Revenge Spending”

Many shoppers are waiting to splurge after restrictions are lifted, and this “revenge spending” will boost sales in several industries. We are already starting to see the revenge spending trend in post-lockdown China, with the luxury brand Hermes alleged to have seen US$2.7 million in sales at their flagship store in Guangzhou just a day after reopening.

Numerous luxury retailers in Hong Kong and China are noticing a gradual bounce back; however, they are seeing a shift in consumer trends in response to the crisis. These changes include:

- More luxury purchases happening in China rather than abroad, due to travel restrictions.

- More customers making online purchases instead of returning to the stores in person.

- More concern about sustainability and the end-to-end product life cycle.

- A “post-aspirational” mindset where ethics are as important as aesthetics – leading to a shift towards purposeful brands.

Sectors most likely to benefit from revenge spending:

- Online education (e-learning) service providers: Demand here will be two-fold. Professionals will be looking to improve and expand on their skill sets as the job market transforms. Meanwhile, parents looking to make up for lost time in their children’s education will be more likely to invest in quality online learning.

- Sports and physical wellness: Consumers will be eager to return to gyms and fitness centres after being at home. Sports equipment and facilities are expected to see a rise in demand.

- Health care and pharmaceuticals: Families will be stocking up on supplements and replenishing their first-aid kits in anticipation of future events like the COVID-19 lockdown.

- Consumer electronics: These “non-essential” items will see a surge when they become available to purchase again. More consumers will be looking to upgrade or replace faulty electronics after the lockdown. Many will also be looking to set up more reliable telecommunication systems, to make remote working easier in the future.

- Logistics: More spending on imported products will lead to an increase in shipping demands.

It is predicted that the majority of this buying will be done online. Consumers will have grown more comfortable with virtual shopping and virtual entertainment, such as streaming movies and live events.

Some Sectors Can Expect a Slower Recovery

Even after lockdown and travel bans are lifted, it is likely that crowded spaces like shopping malls, cinemas, markets and sports stadiums won’t be visited as frequently. Consumers will also be less likely to travel unnecessarily, and fewer will want to stay in hotels. This means the entertainment, hospitality and tourism sectors will be slower to rebound.

What Makes a Resilient Industry?

The industries that have experienced the least disruption – and will likely see the quickest recovery – are those which have at least one of the following in place (or which can adjust to make the following possible):

- Ability to work from home

- Scope for rebound

- Use of temporary employment contracts

- A robust online business model with a focus on business continuity

Let’s look at a couple of examples of this, specifically in retail and business services.

Resilience in Retail:

The retail sector can make use of temporary contracts to reduce overheads, and the rise of e-commerce is giving the industry better scope for a rebound. Some retailers are also experiencing a surge in demand as buyers stock up on food products and other essential items, for fear of possible future shortages.

However, other retailers (mostly non-food retail) are seeing a drop in business. Some customers feel safer staying home, some are concerned about their future income, and some shops have been required to close temporarily during lockdown. Retail chains that do not have online stores or click-and-collect options have experienced the most severe losses – Primark being one key example.

Retailers have been affected by capacity limitations in freight transport between China and Europe. Shoppers are delaying the purchase of larger items and luxury goods until stores begin operating as usual again.

Resilience in Business Services:

Advances in telecommunication mean the majority of the business service industry now has the ability to work remotely. This means the sector has the potential to rebound well and to adapt to future challenges.

Meanwhile, demand has fallen for “support services” like cleaning, catering and security. Data centre services and video conferencing providers are seeing a significant surge in demand as more businesses turn to these online applications.

Looking at the predictions from China and the trends emerging around the world, we can expect the most adaptable industries to bounce back the fastest, especially those that enable consumers to buy products, services and experiences digitally rather than physically.

Looking for Office Space?

We Operate in Some of the World’s Top Cities:

London, New York, San Francisco, Paris, Singapore, Hong Kong,

Search more locations