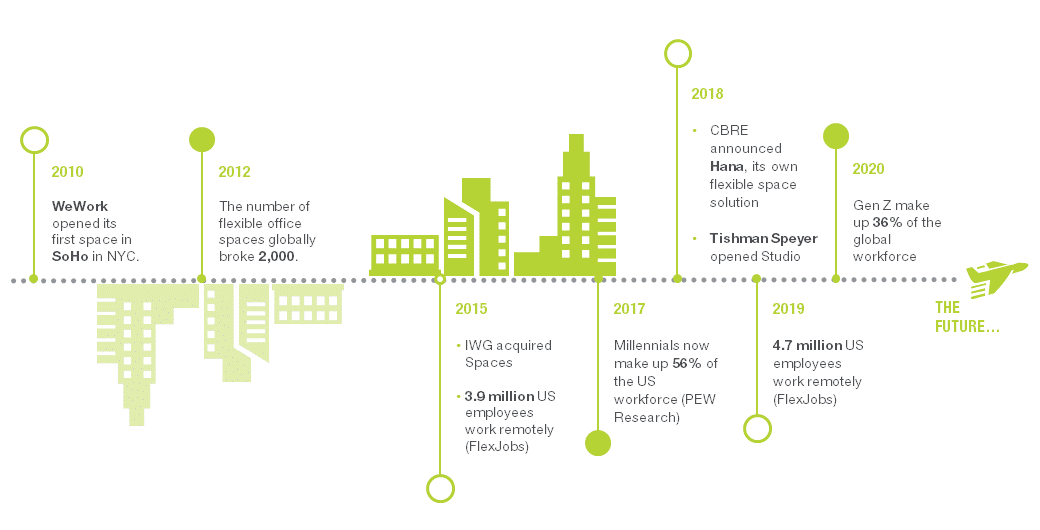

The past decade in commercial real estate can be defined by one word: change. And the changes, stemming from how we work, technological advancements and economic influence, have brought flexible office space to the forefront of Commercial Real Estate (CRE).

As a younger generation joins the workforce, technology enabling remote working and the retention of talent has become increasingly important. Expectations of office space have evolved to the point that the flexible office market is now focused on providing a service, rather than an easily commoditized product.

Market Overview

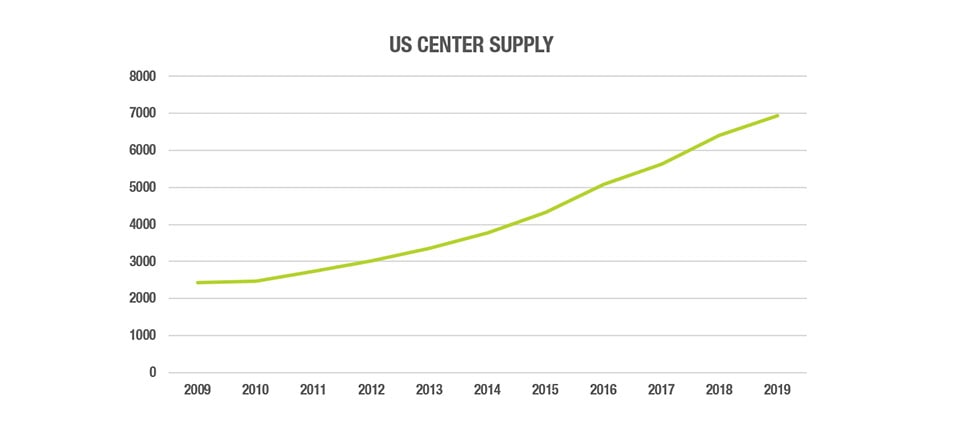

The number of flexible workspace centers in the U.S., including coworking, hybrids and large suites, has almost tripled over the past ten years. In the first half of the decade, we saw a growth rate of 55% for all types of flexible office space, and a particularly impressive growth rate of 198% for coworking centers. The second half of the decade saw a rise in all flexible office types, but primarily hybrid centers, consisting of both private offices and coworking space. The market was evolving to meet changing client demand for a different variety of flexible workspace.

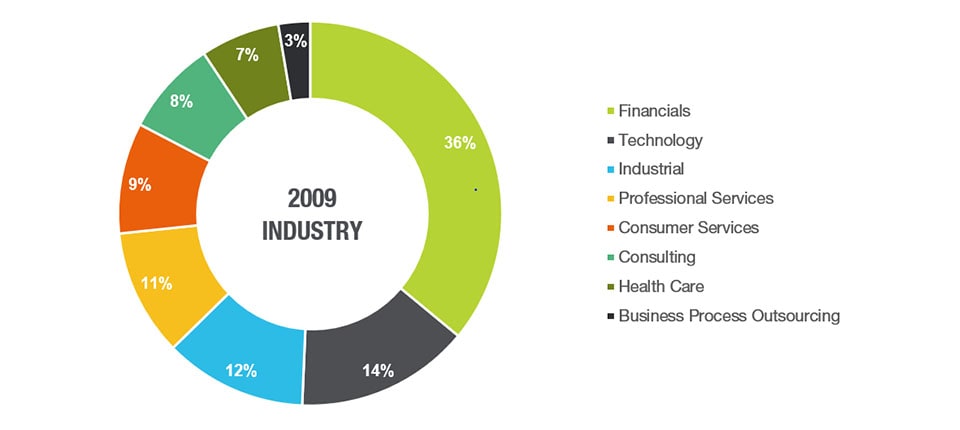

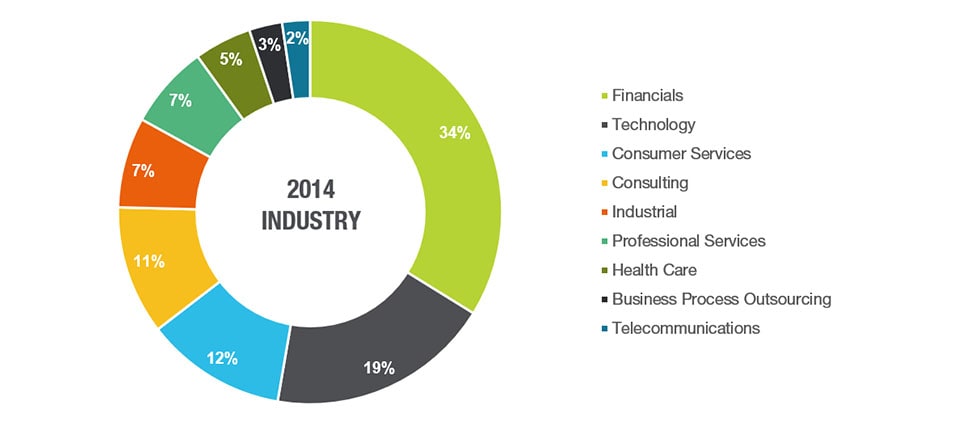

In 2009, out of the 2435 centers in the US, 65% were pure serviced space, defined as a fully equipped office managed by a provider, just 5.8% were purely coworking, meaning space that is entirely shared. In 2019, 42% of centers were purely serviced and 15% were purely coworking. This decade marked not only the increase in popularity of flexible office space but also a shift in the market to focus more on the end-user. Workspace-as-a-service popped up as a term in the latter part of the decade – defined as office space that is completely tailored and customized to the client’s needs but procured on flexible terms.

As the office environment begins to embrace remote working, flexible office centers are moving to secondary and tertiary markets across the US. In 2015, 50% of the total flexible office market was located in five states – Florida, Texas, New York, Illinois and California. Although these states are still the market leaders, we’re seeing the highest growth in supply of flexible workspace in the secondary markets of District of Columbia, Georgia, Ohio, Maryland and Virginia.

The Consumer

The industry at times is still perceived as made for the start-up; small firms that need a launchpad or use flexible office space as an alternative for working in a coffee shop. Although this type of end-user is still seen throughout flexible workspaces, the consumer mix has diversified in the last decade.

While 1 to 2 desk requirements still dominate the market, it is no longer uncommon to receive a requirement for 25 or more desks. It is no longer surprising to see large firms moving their main office from traditional leases to flexible office leases, specifically under the workspace as a service model. Predominantly, however, larger firms use flexible office space for satellite offices or remote employees which combined with the start-ups using the office space, explains why the 1-2 person office has dominated the market throughout the entire decade. In 2009, 74% of transactions were 1-2 workstations; whereas in 2014, the number increased to 75% and in 2019 to 78%.

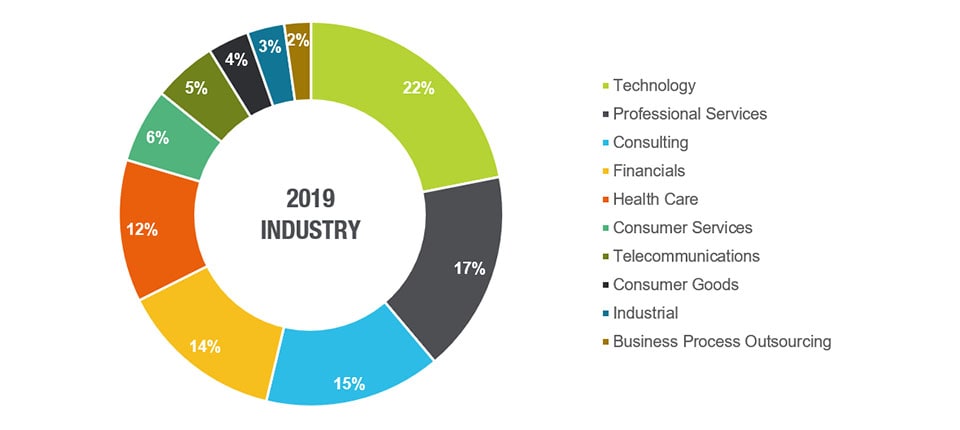

Embracing flexibility by industry…

While TAMI firms – technology, advertising, media and information companies – have typically gravitated towards a conventional office lease due to their need for more collaborative open spaces, the workspace-as-a-service model allows for a customized space without the risk of a long-term lease. In 2019, technology firms led the way in acquiring flexible office space, a spot that has been reserved for financial firms since 2009.

Embracing the Service Model

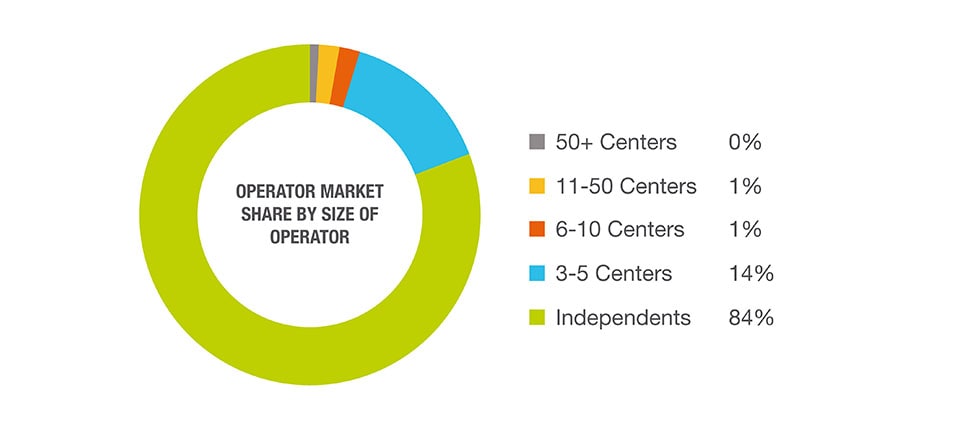

We can partially credit the growth in the supply of flexible office space to the large players, such as IWG and WeWork, who in particular dominated the news cycle at the end of the decade. However, perception is not reality in this case. The flexible office industry is largely made up of small, niche providers. At the close of the decade, 84% of flexible space providers were independent operators with one or two locations. These niche providers, in particular, focus on core community values and often remain closely aligned to the “coffee shop” view of coworking. With the growth in availability, location is no longer a selling point. Tenants are making decisions based on community values and service provisions as the market shifts from selling a product to selling a service.

As the market gains momentum, competition has greatly increased – not only from new providers but also from landlords and brokerage houses who have made it clear that they won’t be left out. Landlords have started adding flexible office spaces into their assets either through partnering with or acquiring an existing provider, or creating their own flexible office arm. By the end of the decade, industry heavyweights such as Blackstone Group, Tishman Speyer, Related and Boston Properties have all entered the workspace-as-a-service market. Brokerage house CBRE introduced their flexible workspace solution Hana to the market in 2018. To combat the competition and find an easier transition into secondary markets, IWG, Venture X, Office Evolution and many more have embraced a franchise model.

Forecasting the Next Decade

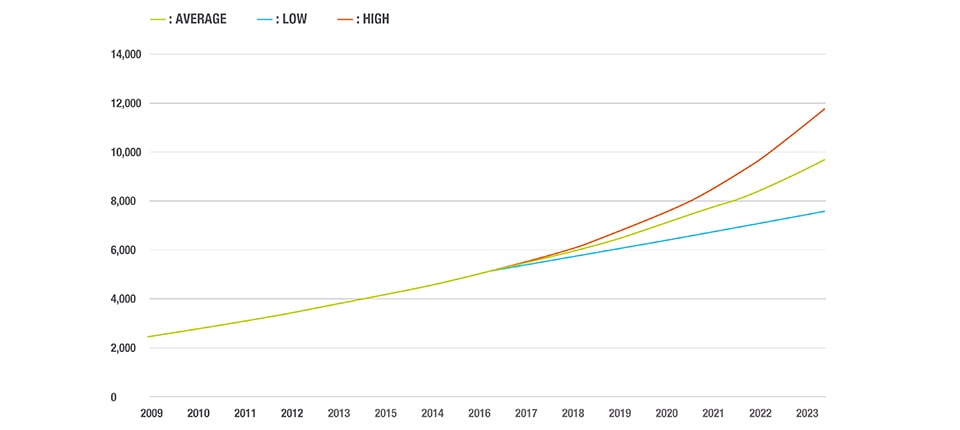

As competition and demand continue to increase, we predict that we can see upwards of 10,000 flexible office locations across the US by 2023, an increase of more than 3,000 locations. If we build out the trends that we can see in our data from the previous decade, we will see this growth being driven by larger companies from a variety of sectors adding flexibility into their real estate portfolios in order to avoid the risk that comes with a conventional lease.

The market mix will become more diverse – with more operators being joined by a mix of landlords, and not just those from office space, as retail and other property sectors will get into the act of providing flexible workspace. Center supply will increase through competition with new players already coming into the market and growing rapidly in secondary and tertiary markets. This supply will be driven by demand for more flexible workspace options in the states outside the largest five markets where the current proportion of flex space as a percentage of total CRE space is still in low single digits.

Click to enlarge

Looking for Office Space?

We Operate in Some of the World’s Top Cities:

London, New York, San Francisco, Paris, Singapore, Hong Kong,

Search more locations