The growth of flexible workspace is set to spread to new markets in 2019.

The flexible workspace sector has ridden the crest of a wave for the past five years with global demand increasing by 50% and more market supply of flex space than ever before. Instant now estimates the global market to incorporate 32,000+ centres, which represents 521 m sq. ft. This is an increase of 15% year on year since 2013.

2018 showed significant market shifts with an increase in corporate clients looking for flex space. Demand from corporates increased by 21% in 2018 alone. Landlords are also taking a greater interest in the sector in the face of this increase of client demand.

But what will happen in 2019?

Flexible Workspace Trends for 2019 and Beyond

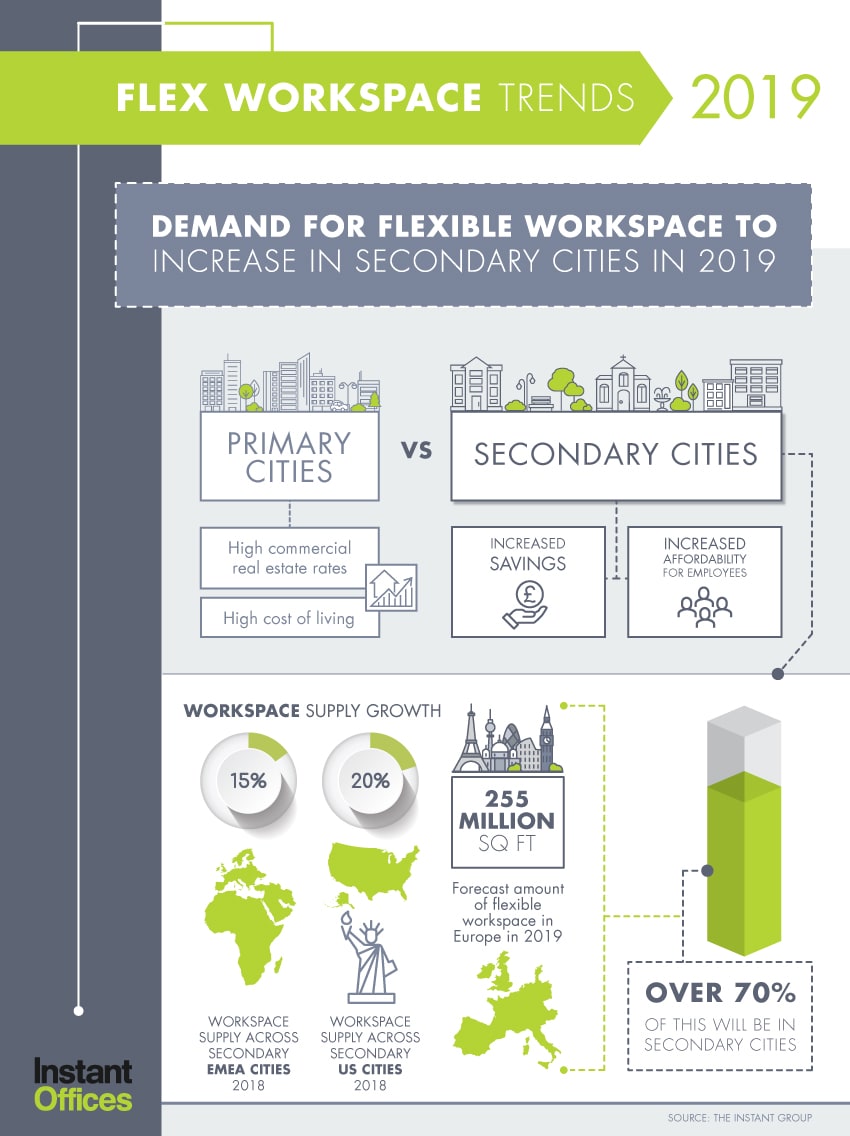

Demand is set to expand outside of the primary global city-based markets.

- Occupiers continue to reassess the way they use office space, and with both commercial real estate rates and the cost of living some of the highest on record, many companies are starting to look towards secondary cities to cut costs and increase affordability for employees. Forbes announced that the fastest growth markets in the US (gross metro product) in 2018 were Las Vegas, Orlando and Austin, all secondary markets, while in Europe, Manchester and Toulouse topped the UK and French markets thanks to increasing investment and a growing corporate focus.

- All EMEA cities, including Manchester, Lille and Frankfurt, have seen supply grow by 15+% in response to accelerated demand. In the US states such as Kansas, Nebraska and Oklahoma, all reported growth rates of over 20% across the last 12 months. (A detailed insight on this will be available in Q1)

- Europe is forecast to see 255 million sq ft of flexible space in 2019 – a 12% increase with over 70% of this space being available in smaller secondary cities.

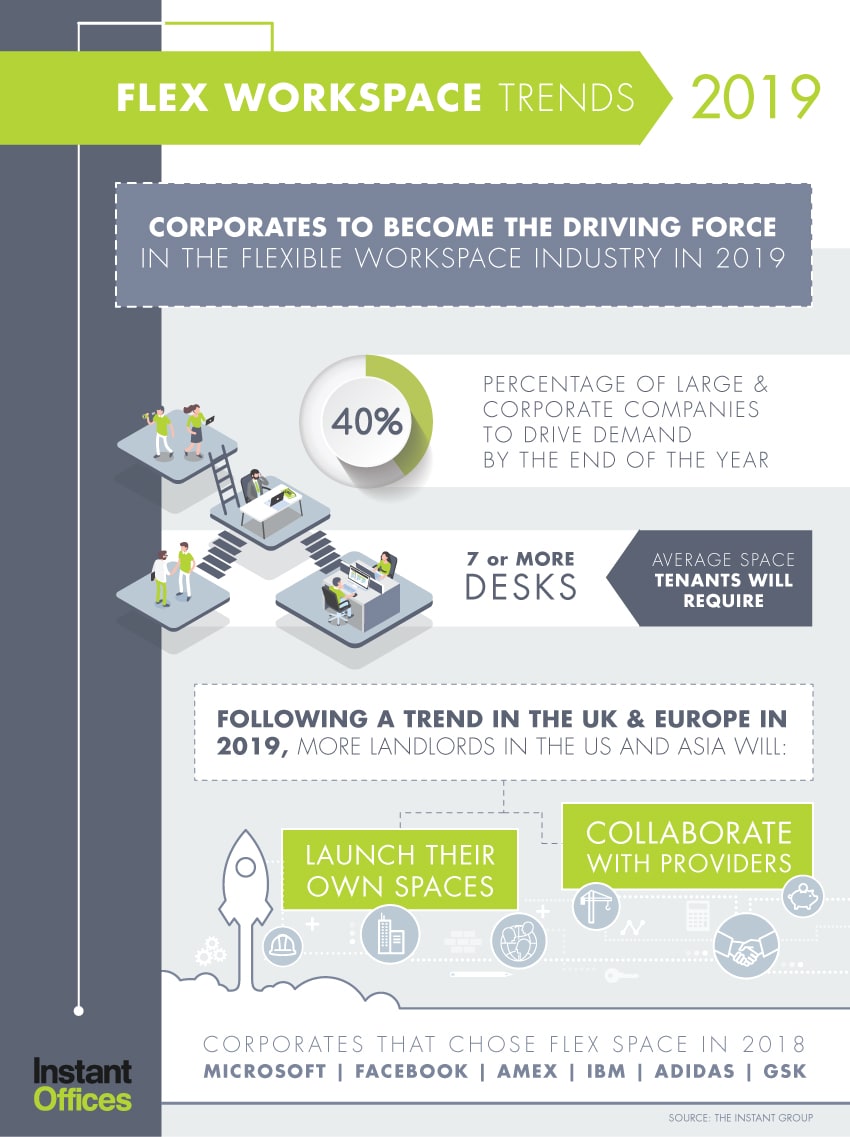

Corporates are set to become the driving force within the flexible workspace industry as the way they view their office portfolios continues to change.

- By the end of 2019, 40% of demand is forecast to come from large and corporate companies, with the average tenant taking seven or more desks in flexible space.

- Corporate organisations are looking for larger and more agile workspaces, which is symptomatic of a global move towards more flexible lease terms. The ‘Space as a Service’ model was responsible for some of the biggest flex deals of 2018 in New York and London and included household brand names like Microsoft, Amex, IBM, GSK, Adidas, and Facebook.

- On the back of corporate tenant pressure, increasing numbers of landlords in the US and Asia will launch their own spaces or collaborate with providers. We’ve already seen this trend in the UK and Europe, but it is yet to take off in either of these markets.

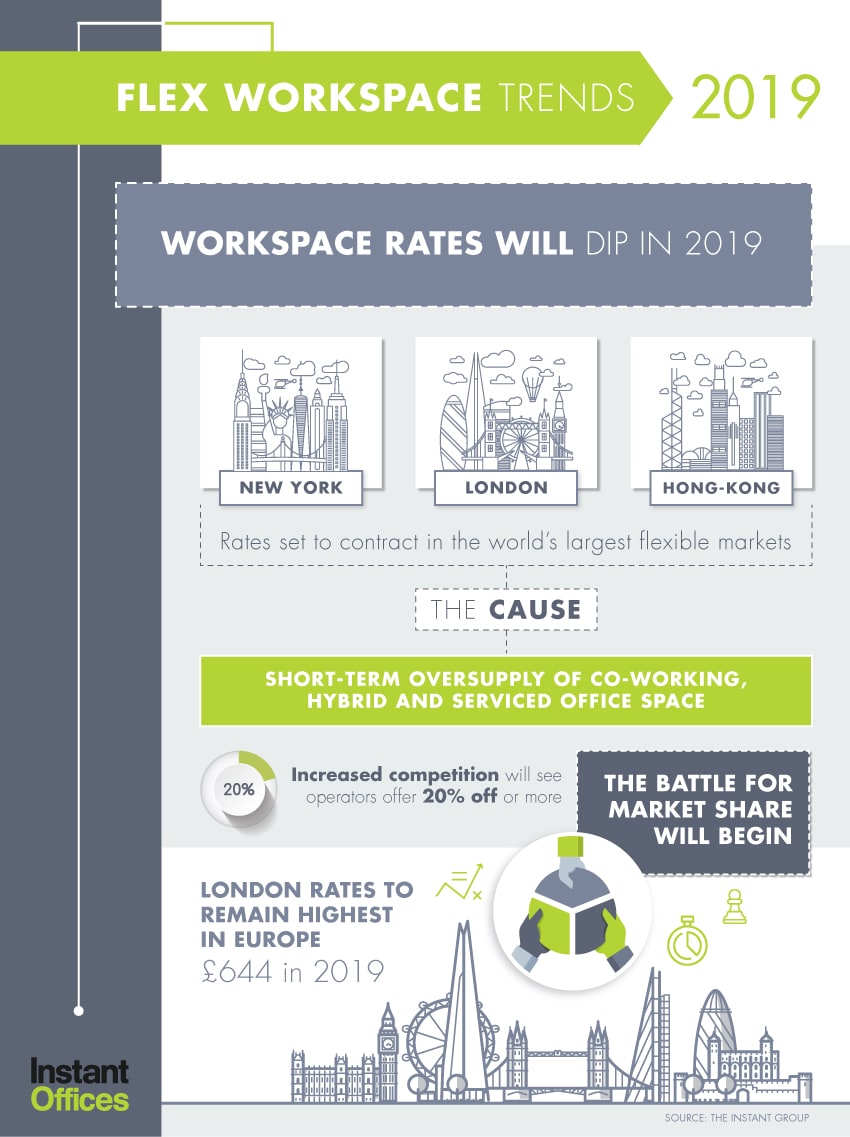

Prices are set to flatten in some of the largest flexible workspace markets despite increasing demand.

- Despite growing demand, short-term oversupply of all types of flexible office space including co-working and hybrid will see 2019 rates contract in London, and we expect to see the same trend follow in New York and Hong Kong – the world’s largest flexible markets.

- As the type of demand changes and the lifetime value of occupiers in flexible space increases, leading operators are expected to become more competitive and offer increasing discounts in key markets to gain share. We forecast that in these competitive markets operators will be willing to offer 20% or more off the advertised rates while they attempt to gain market share.

- London rates are forecast to remain the highest in Europe at £644 in 2019 (despite the flattening of pricing mentioned in #2), which alongside strong demand means suppliers continue to move into the market. We expect to see the flexible market make up 7% of the London CRE market in 2019 on the back of continued investment and growth.

Looking for Office Space?

We Operate in Some of the World’s Top Cities:

London, New York, San Francisco, Paris, Singapore, Hong Kong,

Search more locations